Hope you all had a happy Easter weekend. This was an extremely unorthodox Easter weekend with separated families and social distancing, however there are some positives to report (minus the cheap Easter eggs).

Q1 2020 brought on the first-time renewables overtook fossil fuels to become Britain’s main source of power, mainly thanks to the influx of weekly named storms which battered the UK over this period, leading to record breaking winds. This was the main factor for an increase in renewable generation of 30% from Q1 2019. Hopefully much more of this to report in the future.

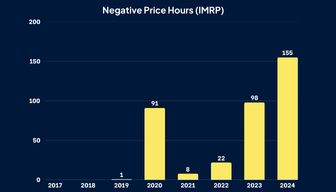

Last weekend had strong wind and solar generation, and reduced electricity demand causing negative pricing for 4 consecutive hours, one of the longest periods recorded. This was once again the case for Easter Monday, as high wind generation and low demand meant System Sell and N2EX prices went negative for considerable periods of time.

This lowered electricity demand has been caused by the imposed lockdown and the jump in people working from home. In day electrical demand has fallen almost 20% since the COVID-19 lockdown. It is also worth mentioning that day ahead prices fell 10% week on week and 30% year on year with this also being the main driving factor.

We haven’t done a report in a while due to current news, however here is the fall in almost a month for Winter ‘20.

See below for a PPA valuation of a 1MW PV asset from the Renewable Exchange Marketplace forecasting tool since 14th March 2020.

To find out more about our products and services please email [email protected] or register to access the platform today.