As the lockdown continues and social distancing slowly becomes the norm across the globe, we see the destructive effects that low demand has caused on UK and Global power markets.

Over the past 28 days only 0.7% of our power has come from coal, driven by low demand, low gas prices, and coupled with very high PV production alongside higher wind production for this time of year. This unexpected high PV output caused negative system sell and day ahead prices, spelling bad news for solar generators selling on indexed contracts with a low of -£19/MWh recorded on Sunday 5th April. Day ahead pricing for the month of April averaged at £24.18/MWh compared to £43.35/MWh for April in 2019. Low prices are set to continue with baseload for May closing at £24.60/MWh yesterday.

UK power is currently going through its longest coal-free period since 1882, starting on April 10th 2020 and currently is at 20 days straight. Last year only 2.5% of UK power came from coal, with all coal power stations set to close by 2025 in the UK. Reduced power demand and low gas prices are the cause, but 20 coal-free days is nevertheless an outstanding milestone in the transition to a low carbon fuel mix.

Also in positive news the clap for NHS workers on Thursdays are seeing spikes in electricity demand as people go back inside and turn their TVs and kettles on. Today is likely to follow suit!

With the next UK COVID lockdown review occurring in a weeks’ time it will be interesting to see how the announcements will impact the UK and European Power markets.

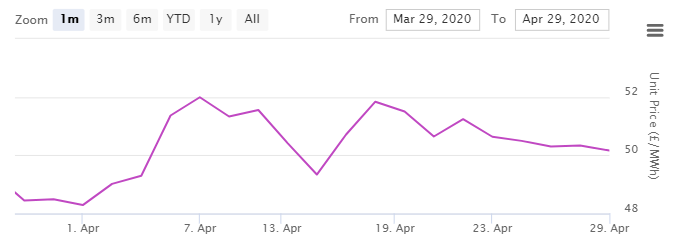

See below for a PPA valuation of a 600kW Hydro asset from the Renewable Exchange Marketplace forecasting tool since 29th March 2020.

To find out more about our products and services please email [email protected] or register to access the platform.